Darwin, Risk Managers

& the Global Financial Crisis

In 2008, after many years in the making, the financial crisis we now all know so well finally erupted in the United States. But how—and why—did it spread to other countries and ultimately become a global crisis?

The growing economic interdependence between the U.S. and the rest of the world, combined with the broad global diffusion and liberalization of trade, transactions, social structures, technology, culture, political systems, knowledge, and science, has created a powerful force pushing toward global convergence—a shared, interconnected reality. This is what we commonly refer to as globalization.

From 2008, when the crisis first emerged in the U.S., until 2011, when it matured, deepened, and—through globalization—spread to other advanced economies, the phenomenon could no longer be described as a national or regional event. It had become a global financial crisis.

From 2008, when the crisis first emerged in the U.S., until 2011, when it matured, deepened, and—through globalization—spread to other advanced economies, the phenomenon could no longer be described as a national or regional event. It had become a global financial crisis.

It is clear that every crisis generates both new opportunities and new threats. It reshapes the global order, triggering rapid and often shocking changes that demand adaptation. In doing so, it confronts the international community with what may be one of the most complex environments it has ever faced.

“But what, ultimately, is a financial crisis?”

Risk management professionals argue that if organizations had been equipped with effective risk management functions, structures, and processes, the recent global financial crisis might never have occurred.

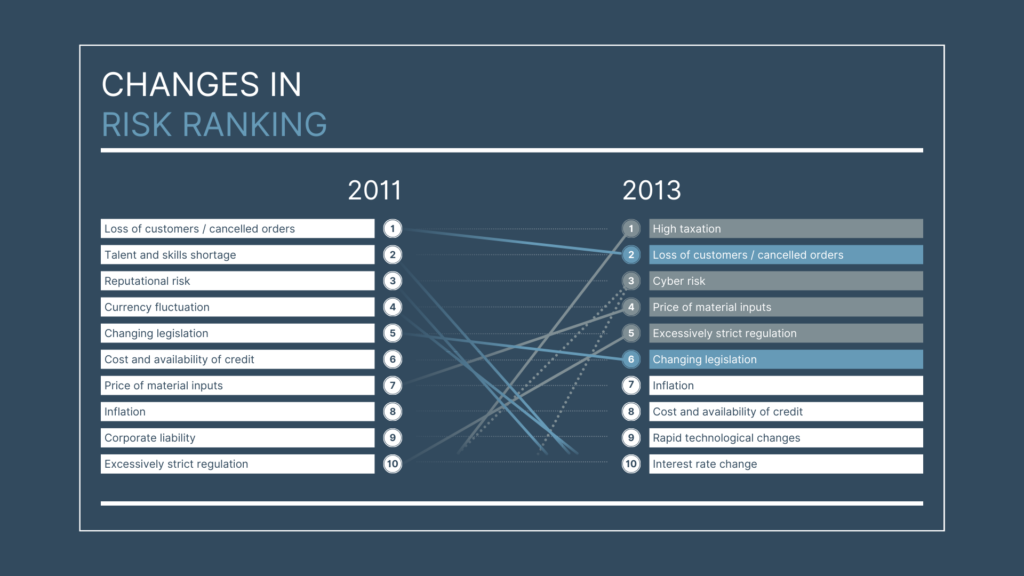

Through specialized risk reports published annually by international risk-focused institutions, we can observe how risk landscapes evolved before and after the crisis. One such report by Lloyd’s of London illustrates the top ten risks threatening financial organizations worldwide. Prior to the crisis, this top-ten risk ranking was remarkably stable—so stable, in fact, that even the order of risks remained largely unchanged.

After the crisis reached full maturity in 2011, however, the risk environment shifted dramatically. Risk managers around the world maintain that the financial crisis was essentially the result of organizations’ collective inability to respond to and adapt to changing risks.

Change is inevitable—especially within the highly complex ecosystem of today’s globalized economy. But could it be that the greatest challenge of all lies in an organization’s capacity to adapt rapidly to these changes?

Perhaps Darwin’s famous observation applies just as powerfully to modern economics as it does to biology:

“It is not the strongest of the species that survives, nor the most intelligent, but the one most responsive to change.”

And perhaps this insight offers one of the clearest explanations of the global financial crisis itself.